Telecoms Access Review 2026-31

17 December 2025

About UKCTA

1. This submission is made by the UK Competitive Telecommunications Association (UKCTA). UKCTA is a trade association promoting the interests of fixed line telecommunications and broadband companies competing against BT as well as each other, in the residential and business markets. Its role is to develop and promote the interest of its members to Ofcom and the Government. Details of membership can be found at www.ukcta.org.uk. Its members serve millions of UK consumers.

Introduction

2. Leased Lines provide the communication backbone to UK enterprises and thepublic sector. They provide backhaul to mobile sites and while they are largely invisible to end consumers, their necessity cannot be overstated. While much of the focus in the TAR (and the WFTMR before that) is on FTTP, traditional business connectivity is market that requires regulatory oversight, to ensure UK consumer have access to a range of services and that were significant market power exits it is remedied appropriately.

3. UKCTA members have significant interest in this market, either through selling business connectivity services in competition to Openreach in some geographies, to being purchases of this kind of connectivity to supply the enterprise sector or to support their own backhaul needs.

Considerations when deciding an appropriate Buffer Distance

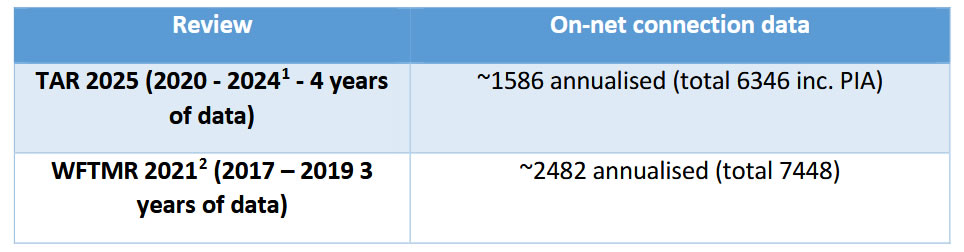

4. The buffer distance represents the extent to which an alternative leased line network builder will extend their network to reach a new enterprise premise. Such network extensions have been in long-term decline.

• 2017–2019: The average annual network extension rate was approximately 2,482.

• 2020–2024: Despite the use of both new duct construction and Openreach’s duct and pole infrastructure, the annual construction rate fell significantly to around 1,586, compared to the previous period.

6. This trend highlights that propensity to build is as critical as the distance itself when assessing network expansion behaviour.

7. Ofcom should be mindful that an extended buffer distance is only a proxy for potential competition and does not, on its own, demonstrate that customers in those postcodes actually benefit from multiple, effective suppliers.

8. Physical proximity within 75–100m may overstate competitive pressure where rival networks are technically nearby but not connected to sites, lack wayleaves, or would face uneconomic build costs to connect all but a few anchor tenants.

9. Ofcom should be clear that there are other compelling factors that need to be assessed in order to determine whether there is, in actual fact, material and sustainable competition. UKCTA are keen advocates of pro-competitive, pro-investment outcomes, but key factors such as the financial strength of rivals networks, their scale and extent of interconnection as well as go to market focus are also import and considerations that have a bearing on competitive outcomes for consumers of these important services.

Approach to Glidepaths

10. Ofcom’s general preference for glidepaths should not be applied in the case of lead-in price Charge Control caps, as the rationale for this preference are not applicable 4 UKCTA Secretariat 251217 in this case. The proposed lead-in price reduction is not driven by Openreach efficiency gains or other considerations to influence forward-looking incentives for Openreach’s behaviour, but instead a revised cost attribution methodology based on Ofcom’s further analysis.

11. The lead-in price change reflects Ofcom’s recognition that the WFTMR approach risked over-recovery by Openreach due to CPs leaving fibre in situ post-churn. This is a correction of a structural misallocation, not a reward for cost reduction.

12. Ofcom’s own Charge Control design principles support Starting Charge Adjustments where prices are significantly misaligned with costs for reasons unrelated to efficiency. That condition is clearly met here.

13. A glidepath would delay the correction of a known distortion, prolong above-cost price levels and undermine economic efficiency and competition; this is precisely the scenario Ofcom identifies as warranting a Starting Charge Adjustment.

Impact on PIA

14. Artificially elevated lead-in prices during the early years of the control period could suppress PIA-based CP volume growth, contrary to Ofcom’s stated objective of promoting competitive fibre rollout and a level-playing field.

15. Ofcom’s general concern about price discontinuities would not materially arise in this case. The SCA would align prices with the long-run efficient level already anticipated by Ofcom’s glidepath trajectory, providing greater predictability and clarity from the outset. Furthermore, the full range of Ofcom’s indicative low/base/high scenario prices modelled for 2030/31 are broadly consistent (or above) the lead-in charges that were in place in 2020/21 and so rather than a disruptive step-change in prices, and Starting Charge Adjustment would be a prompt reversion to pricing levels when PIA CPs entered the network competition market.

16. Furthermore, a Starting Charge Adjustment would not undermine Openreach’s incentives and should not impact on its behaviour regarding PIA. The price change does not penalise efficiency and instead ensures fair cost recovery and supports correct pricing signals for CPs during a critical period for take-up and network expansion.

17. In light of the above, Ofcom’s own framework and the specific circumstances of the lead-in charge change point to a Starting Charge Adjustment as the proportionate and analytically justified approach that ought to be adopted in TAR. The integrity of Ofcom’s decision making and BT’s Regulatory Financial Reporting.

18. UKCTA members have very significant concerns over the circumstances that have led to the proposed attribution changes within BT Regulatory Financial reporting structure, which have a directly impact on the integrity of Ofcom’s concluding work on the Telecoms Access Review.

19. The timing and rationale for these attribution changes raises important questions regarding the robustness and integrity of the process. This is particularly relevant given that Ofcom appears to be willing to accept the transfer of a substantial portion of costs from one market, which is subject to a comprehensive charge control remedy intended to address market failure in leased line supply, to another market, where BT does not face similar cost-based charge controls and the Regulatory Financial information only serves a contextual purpose, lacking any direct implications for price setting.

20. UKCTA members should not need to remind Ofcom of the very significant information asymmetry that exists, which enables BT to selectively implement modifications to its regulatory financial reporting in ways that serve its own interests, particularly in situations where there is limited transparency regarding both the methodology and any alterations made to it. The change control documentation which presents the change (in order to justify a +£90m in attribution change) only has three pages of meaningful content, completely lacking the detail found in the accounting methodology. The document does make clear that the motivation behind the change is ‘BT’s Judgement’.

21. Over a decade ago, industry observed several instances in which BT restated or reattributed costs within their Regulatory Financial Statements (RFS), with these actions driven by an intention to optimise commercial returns for BT Group, resulting in regulatory outcomes that were more favourable to BT than if attribution decisions had been made independently of commercial considerations. In the period between 2008 and 2011 there were five significant instances of restatements by BT of the numbers within its RFS, and / or of material changes being made to its valuation assumptions:

• In September 2008, BT restated the volume and revenue data relating to PPC services contained in its 2006/7 RFS (reducing revenues by £143m)

• In the same year internal revenues attributable to AISBO services (covering Ethernet) were also restated.

• In July 2010, BT’s regulatory financial statements showed a significant increase in the net replacement cost of duct and copper access network assets vis-à-vis the previous year, with BT increasing the value of its assets by £1,880 million.

• In September 2011, BT took the decision to review the methodology it used to calculate the LRIC, DLRIC, and DSACs for its RFS for 2010/11, and restated these figures for 2009/10.

• In the same year, BT’s RFS for 2009/10 were also restated “to reflect a correction in BT’s calculation of internal links volumes” in the TISBO market.

22. Undaunted, in the 2013 RFS, BT introduced a large number of changes in attributions. The impact was twofold: firstly, ~ £90m of cost was reattributed from unregulated products to regulated products and secondly, costs were reattributed amongst regulated products and in particular £76m of cost was reattributed from business connectivity products (where the market review had recently closed and the charge control locked down) to local access products (where the market review was ongoing and charge control was yet to be set).

23. Faced with this endless cycle or restatement and reattribution and clear manipulation, Ofcom finally lost patience, deciding to disregard BT’s 2013 changes in totality, recognising that they were motivated by an attempt by BT to game the regulatory system. Regrettably, after a period of stability we now find ourselves in a position remarkably similar to 2013/14, with BT yet again changing the numbers to, undermining Ofcom’s work and seek a more favourable regulatory settlement.

24. We would urge Ofcom to act with the same integrity and courage as it did in 2014 and reject BT’s October 2025 commercially motivated attribution changes. Ofcom cannot protect the consumer interest if it presides over a system that can be so easily manipulated by a dominant firm at this stage in a market review process.

25. The outcome of the changes has a material impact on end pricing. By moving £78m of costs out of broadband where costs were recoverable across ~24M users to leased lines where costs are recoverable by just ~105k businesses, the cost burden moves from ~£3 per household to ~£750 per premise. A change of this magnitude needs very carefully consideration and Ofcom appears to have accepted it without proper scrutiny.

26. When attribution changes are commercially motivated and not instigated as part of an unbiased, wider attribution review, the integrity of the regulatory decision-making process is called into question.